Life insurance death benefits remain completely exempt from taxation in Canada. Named beneficiaries receive life insurance proceeds entirely tax-free under federal tax provisions governing Canadian insurance contracts. Throughout 2023, Canadian families collected approximately $14.7 billion in tax-exempt death benefits from life insurance policies, securing crucial financial protection during periods of loss and transition. Tim Cestnick, Managing Director of Advanced Wealth Planning at Wellington-Altus Private Wealth and distinguished tax columnist for The Globe and Mail, emphasizes: “The tax-exempt status of life insurance death benefits delivers one of the most powerful financial advantages available in Canadian tax planning, particularly when contrasted with registered assets and capital properties that trigger substantial deemed disposition taxes at death.”

While death benefits escape taxation entirely, specific circumstances generate tax consequences within life insurance arrangements.

Permanent life insurance policies accumulate cash values through tax-deferred growth mechanisms, yet policy redemptions trigger taxable income on amounts exceeding adjusted cost basis thresholds.

Corporate-owned insurance policies unlock specialized tax advantages through Capital Dividend Account mechanisms, enabling tax-free distributions to shareholders from death benefit proceeds. Canadian private corporations maintained approximately $95 billion in corporate-owned life insurance throughout 2023.

Policy loans accessed from permanent insurance generate no immediate tax liability upon receipt, though unpaid loans at policy maturity can trigger adverse tax consequences.

Participating policy dividends flow to policyholders tax-free up to adjusted cost basis limitations.

Policy ownership transfers between parties can initiate taxable disposition events requiring careful tax planning.

The comprehensive tax treatment depends on policy classification, ownership structures, and benefit distribution methods. Term life insurance policies involve minimal tax considerations beyond tax-exempt death benefits. Permanent insurance products—whole life and universal life—face government-imposed restrictions on tax-deferred accumulation while offering potential tax-free access to policy values through strategic design implementation.

No, Canadian life insurance death benefits escape taxation entirely. Named beneficiaries receive life insurance proceeds completely tax-free under federal tax statutes governing insurance contracts. Canadian families collected approximately $14.7 billion in tax-exempt death benefits throughout 2023, securing essential financial stability during challenging circumstances. Tim Cestnick, Managing Director of Advanced Wealth Planning at Wellington-Altus Private Wealth and recognized tax authority for The Globe and Mail, states: “The tax-free nature of life insurance death benefits represents one of the most valuable attributes of these financial instruments, especially when compared to other estate assets that generate significant tax liabilities through deemed disposition rules at death.

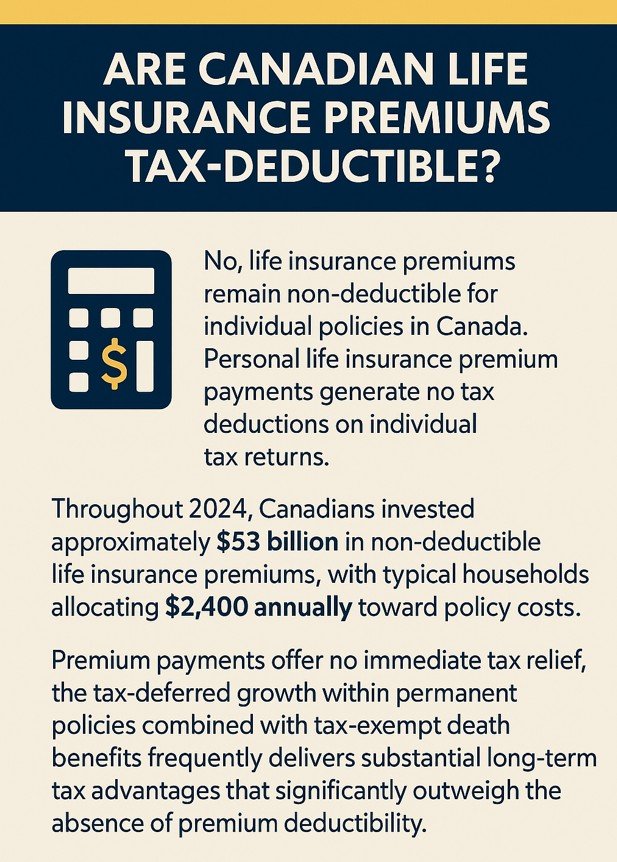

Canadian life insurance premiums for individual policies are not tax-deductible, meaning that individuals cannot deduct these premium payments on their personal tax returns. In 2024, Canadians will pay approximately $53 billion for non-deductible life insurance premiums, with the average household spending $2,400 per year on policy expenses. According to Jamie Golombek, Managing Director of Tax and Estate Planning at CIBC Private Wealth, while premium payments are not deductible in the short term, the tax-free growth in permanent policies and tax-free death benefits create significant long-term tax savings that outweigh the lack of premium deductibility.

Term life insurance generates minimal tax implications while permanent life insurance delivers extensive tax advantages. Term policies provide exclusively tax-exempt death benefits without investment components, whereas permanent policies enable tax-sheltered accumulation alongside potential tax-free withdrawals from policy values. Permanent insurance policies across Canada contained approximately $340 billion in tax-sheltered cash values throughout 2024, appreciating at an average annual rate of 5.8%* while remaining completely sheltered from annual taxation. Kim Moody, Director of Canadian Tax Advisory at Moodys Tax Law LLP and prominent Canadian tax specialist, notes: The tax advantages embedded in permanent insurance establish it as a critical component in comprehensive financial planning, particularly for individuals who have maximized other tax-advantaged savings vehicles like TFSAs and RRSPs.

No, policy loans from permanent life insurance generate no tax liability when accessed. Borrowing against life insurance policy values creates no immediate tax consequences at the time of loan origination. Throughout 2023, Canadians borrowed approximately $4.2 billion against their life insurance policy values, with average loan amounts reaching $78,000, all accessed without immediate taxation. Mark Halpern, CEO of WEALTHinsurance.com and Certified Financial Planner, explains: Policy loans represent one of the most tax-efficient mechanisms for accessing policy values during the policyholder’s lifetime, provided the policy maintains adequate funding and remains in force to prevent taxable policy lapse events.

Life insurance policy ownership transfers can trigger taxable disposition events. Transferring life insurance policies between related parties or for consideration generates immediate taxation when accumulated values exceed adjusted cost basis. Throughout 2023, the Canada Revenue Agency assessed approximately $225 million in additional taxes from policy transfers where proceeds exceeded adjusted cost basis, with average taxable gains reaching $42,000 per transaction. Wilmot George, Vice-President of Tax, Retirement and Estate Planning at CI Global Asset Management, advises: Policy transfers demand careful analysis of immediate tax impacts balanced against long-term implications for death benefit tax-exempt status, making professional tax guidance essential before executing any ownership transfer.

No, participating life insurance policy dividends remain tax-free up to adjusted cost basis limits. Insurance companies distribute policy dividends as premium returns for tax purposes, maintaining tax-exempt status. Major Canadian insurers paid participating policy dividends averaging 6.5%* of policy values throughout 2023, with the four largest insurers distributing $5.2 billion in tax-free policy dividends to policyholders. Jim Ruta, insurance industry expert and former Investors Group Executive Manager of Life Insurance, emphasizes: Policy dividends deliver one of the most tax-advantaged investment return mechanisms available in Canada, especially valuable in high-tax provinces where investment income faces marginal tax rates exceeding 50%.

Life insurance delivers exceptional tax advantages for estate planning strategies. Life insurance proceeds offset estate tax liabilities triggered through deemed disposition rules while providing tax-exempt inheritance for designated beneficiaries. Life insurance delivers exceptional tax advantages for estate planning strategies. Life insurance proceeds can offset terminal tax liabilities triggered through deemed disposition rules at death, while providing a tax-exempt inheritance for designated beneficiaries. Unlike the U.S. estate tax system, Canada taxes the deceased’s final return on the deemed sale of assets, meaning registered accounts and appreciated capital properties can generate significant tax obligations for the estate. Throughout 2023, the average Canadian estate faced potential tax obligations of $125,000 under deemed disposition regulations, with high-net-worth estates frequently incurring tax assessments exceeding $1.5 million on registered accounts and capital properties including real estate. John Natale, Head of Tax, Retirement and Estate Planning Services at Manulife, explains: Life insurance represents the most cost-effective and reliable method for generating liquidity to satisfy tax obligations arising at death, essentially funding these liabilities for pennies on the dollar compared to actual tax bills.

No, critical illness insurance benefits remain completely tax-exempt in Canada when held personally. Critical illness benefit payments received under personally-owned policies maintain full tax-exempt status under current Canada Revenue Agency interpretations. Throughout 2023, Canadians received $780 million in tax-free critical illness payments, with average benefit amounts reaching $83,000, most frequently paid for cancer diagnoses (62% of claims), heart attacks (19%), and strokes (8%). Brian Burlacoff, Principal of Brian J. Burlacoff Professional Corporation and certified financial planner specializing in insurance strategies, states: The tax-exempt nature of critical illness benefits delivers vital financial protection during medical crises, enabling recipients to focus on recovery rather than financial pressures.

Quebec’s life insurance tax treatment follows federal guidelines while maintaining distinct beneficiary designation procedures. Quebec insurance policies operate under the same federal Income Tax Act provisions while adhering to Civil Code rather than Common Law frameworks. Throughout 2023, approximately 22% of all Canadian life insurance was issued in Quebec, representing $420 billion in in-force death benefit coverage, all subject to identical federal taxation treatment as policies issued in other provinces. Hélène Marquis, Regional Director of Tax and Estate Planning at IG Wealth Management and Quebec tax specialist, notes: While fundamental tax treatment remains consistent across Canada, Quebec’s unique handling of beneficiary designations, particularly through testamentary instruments, requires specialized expertise when implementing insurance planning within the province.

Corporate-owned life insurance contracts deliver significant tax advantages through Capital Dividend Account mechanisms. Death benefits from corporate-owned policies generate Capital Dividend Account credits, enabling corporations to distribute tax-free funds to shareholders. Canadian private corporations maintained approximately $95 billion in corporate-owned life insurance throughout 2023, with average policy death benefits reaching $2.1 million, creating potential Capital Dividend Account credits for tax-free shareholder distributions. Hugh Neilson, Director of Taxation Services at Kingston Ross Pasnak LLP and recognized Canadian tax authority, explains: Corporate-owned insurance represents one of the most tax-efficient mechanisms for extracting corporate value, particularly when integrated with strategic Capital Dividend Account planning that eliminates personal taxation on distributions.

Cash values within permanent life insurance policies accumulate through tax-sheltered growth in Canada. Investment returns within permanent policies—interest, dividends, and capital gains—compound tax-free on an annual basis. Throughout 2023, average participating whole life policies generated dividend returns of 6.2%,* all accumulating tax-sheltered, compared to identical investment returns that would face marginal tax rates reaching 53.53% in provinces like Ontario. Peter Wouters, Director of Tax, Retirement and Estate Planning Services at Empire Life Insurance Company, states: Permanent life insurance represents one of Canada’s last true tax shelters, offering unlimited contribution capacity unlike TFSAs and RRSPs which impose strict annual contribution limits.

Yes, Canadian tax regulations governing life insurance align with Infinite Banking implementations. The Canadian Income Tax Act recognizes permanent life insurance contracts in ways that support Infinite Banking strategies. Federal tax provisions enable tax-free growth within cash value components of whole life and universal life contracts, while policy loans remain non-taxable events when policies maintain in-force status. Nelson Nash, creator of the Infinite Banking Concept, observed: Banking fundamentally concerns the process of financing all purchases, and this process operates effectively within Canadian regulatory frameworks with certain variations from American systems.

Implementation requires strategic structuring to maximize advantages while maintaining compliance with Canadian regulations. Canadian regulations limit policy loans to 90% of cash surrender values compared to 100% availability in the United States, while Modified Endowment Contract rules are replaced by Exempt Test Policy regulations updated in January 2017. Statistics from the Canadian Life and Health Insurance Association reveal that approximately 22 million Canadians owned life insurance policies worth approximately $5.1 trillion throughout 2022, with permanent life insurance representing approximately 37% of all in-force policies.

When developing comprehensive financial plans incorporating life insurance, consult life insurance specialists at IBC Financial. Our advisors deliver expert guidance on all tax implications affecting policy owners. Policy owners must evaluate how life insurance taxation impacts primary beneficiaries and contingent beneficiaries. Insurance carriers like RBC Insurance clarify benefit treatment for beneficiaries upon claim settlement.

Employee benefits including employer-provided life insurance follow distinct taxation rules. Active employees covered under workplace insurance programs may receive taxable benefits for income tax purposes, particularly when coverage exceeds specified threshold amounts. These benefits appear on income tax reporting documents in designated employee taxable benefit categories.

*Note: Dividend rates on participating whole life insurance policies are declared annually by each insurance company based on the performance of the participating fund. Dividends are not guaranteed. Illustrated rates in any policy illustration are not guarantees of future performance. Past dividend declarations are not guarantees of future dividends. The guaranteed values within a participating whole life policy (guaranteed death benefit, guaranteed cash surrender value) are contractually defined. A licensed Financial Security Advisor can provide you with a personalized policy illustration under your specific circumstances.

Take the First Step to Financial Freedom!

We use cookies for analytics & functionality. Manage preferences.

Manage your cookie preferences below:

Essential cookies enable basic functions and are necessary for the proper function of the website.

Google reCAPTCHA helps protect websites from spam and abuse by verifying user interactions through challenges.

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a powerful tool that tracks and analyzes website traffic for informed marketing decisions.

Service URL: policies.google.com (opens in a new window)

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

Google Maps is a web mapping service providing satellite imagery, real-time navigation, and location-based information.

Service URL: policies.google.com (opens in a new window)

You can find more information in our Cookie Policy and Privacy Policy.